Nvidia AI Chips: The Journey from Gaming to Data Centers

The promise around Nvidia AI chips is always clean: rent the GPU, load the model, scale the workload, move faster than the team next door. The first click is less elegant.

That stack is why Nvidia moved from the gaming aisle to the data center floor. The GeForce brand made GPUs familiar. CUDA made them programmable. Hopper made them indispensable for large language models. Blackwell now pushes the argument further: AI infrastructure is no longer a collection of accelerators inside servers. It is a machine-room-scale product, with networking, memory, thermals, software libraries, and procurement politics all fused together.

This is the journey that matters. Not “graphics company discovers AI,” which is too neat. The more accurate version is sharper: Nvidia spent nearly two decades reducing friction between parallel hardware and the people who needed to make it useful. Now the company sells that reduction of friction at data center scale.

The CUDA foundation: when the GPU stopped being just a graphics card

The inflection point was not a keynote about chatbots. It was CUDA in 2006.

CUDA — Compute Unified Device Architecture — gave developers a proprietary parallel computing platform that made Nvidia GPUs usable for general-purpose workloads. That sounds dry. It was not. It changed the interface between software teams and the hardware sitting inside their machines.

Before that, GPUs were powerful but awkward outside graphics. You could admire the throughput, but turning it into useful compute required too much ceremony. CUDA gave developers a more direct route. It lowered the “how do I even touch this thing?” barrier, which is the most underrated barrier in infrastructure.

I still judge AI hardware by that first hour of contact. How fast can a developer move from account setup to running a meaningful workload? How many undocumented edges appear between the marketing page and the first benchmark? How many times does the platform make you feel clever for choosing it, rather than punished for not already knowing its internal weather?

CUDA mattered because it made Nvidia’s hardware feel less like exotic silicon and more like a usable toolchain. Over time, that toolchain became a moat. Framework support, libraries, developer muscle memory, university familiarity, startup defaults — all of it compounded.

This is the part competitors hate, because it is not solved by shipping one good chip. Hardware can be faster on paper and still lose in the first week of developer use if the software path is rough. An accelerator with poor onboarding is not a platform. It is a science project with a purchase order.

Nvidia’s real product was never only the GPU. It was the shortest path from parallel compute to working code.

That is why the evolution of Nvidia AI hardware has to start with software. The chip got the glamour. CUDA got the habit.

From GeForce to Hopper: the data center takes over

The old Nvidia story was easy to understand: gamers wanted better graphics, and Nvidia gave them more frames. GeForce turned GPU upgrades into a consumer ritual. More memory. Better ray tracing. Faster refresh rates. Buy the card, install the driver, launch the game.

AI broke that tidy loop.

Training large models demanded something very different from a gaming card sitting under a desk. It required accelerators built for dense matrix math, high-bandwidth memory, low-latency interconnects, stable drivers, data center thermals, and predictable fleet management. The GPU had to become a unit inside a larger compute fabric.

That shift showed up in the business. Nvidia’s data center revenue surpassed its gaming revenue for the first time in fiscal year 2023. That is not a cosmetic milestone. It marks the moment the company’s center of gravity moved from enthusiast hardware cycles to institutional infrastructure spending.

Hopper, launched in 2022, turned that shift into a product language. The H100 Tensor Core GPU became the shorthand for serious AI training capacity. According to Nvidia’s own positioning, H100 can deliver up to 3x higher performance for large language model training compared with the previous A100 generation. In practical terms, that changed procurement conversations. Teams did not just ask whether they could train a model. They asked how many H100s they could get, when, and at what utilization rate.

The first time I tested an H100-backed cloud instance for model experimentation, the chip was not the only thing I noticed. The performance was there, yes. But the experience depended just as much on scheduling, storage throughput, container compatibility, and network behavior. A fast GPU trapped behind slow data movement is a luxury engine in city traffic.

Here is the cleaner way to frame the transition:

| Era | Primary user expectation | Hardware identity | Main source of friction |

|---|---|---|---|

| GeForce gaming | More visual performance per dollar | GPU as consumer component | Drivers, game optimization, retail availability |

| CUDA expansion | Make parallel compute accessible | GPU as programmable accelerator | Developer learning curve, library maturity |

| A100 generation | Scale deep learning workloads | GPU as data center workhorse | Cluster design, memory limits, cloud access |

| H100 / Hopper | Train and serve large language models faster | GPU as AI infrastructure unit | Quotas, cost, interconnect, utilization |

| Blackwell | Run trillion-parameter-scale systems more efficiently | GPU platform as data center architecture | Power density, cooling, networking, supply chain |

That table hides a harsh truth: each generation solved one bottleneck and exposed a bigger one.

With gaming, the bottleneck was local performance. With AI training, it became memory bandwidth and distributed compute. With frontier inference, it becomes latency, throughput, cost per token, and energy. The user experience shifts too. A gamer sees dropped frames. A developer sees stalled jobs, noisy benchmarks, failed distributed training runs, and bills that do not forgive sloppy architecture.

Hopper made Nvidia the default answer for many AI teams because it matched the moment. It did not eliminate friction. It concentrated the friction elsewhere: into availability, orchestration, and price.

Blackwell and the trillion-parameter pitch

Blackwell, announced in 2024, is where Nvidia stops sounding like a chip supplier and starts sounding like a data center systems vendor with silicon at the center.

The headline number is 208 billion transistors on the Blackwell B200 GPU. The platform is designed to support AI models with up to 1 trillion parameters. Nvidia has also claimed up to a 30x performance increase for LLM inference compared with Hopper. These are large numbers, and they are supposed to be large. Blackwell is built for a market where inference is no longer a side effect of training; it is the product surface users actually touch.

This matters because the economics of AI are moving from “can we train it?” to “can we serve it without setting money on fire?” Training grabs attention. Inference pays the recurring bill. Every prompt, every generated image, every coding assistant completion, every enterprise search query — all of it becomes a latency and margin problem.

When I test AI products as a user, I do not care which accelerator is behind the curtain until the curtain gets slow. Then I care immediately. A chatbot that answers in two seconds feels useful. The same model at twelve seconds feels broken, even if it is technically smarter. A coding assistant that streams smoothly stays in my workflow. One that pauses, hallucinates imports, and then stalls during completion becomes a UI wrapper around impatience.

Blackwell is Nvidia’s answer to that impatience at industrial scale. The platform is not only about raw training muscle. It is about making larger models more economically usable, especially when serving demand spikes and workloads fan out across many GPUs.

The Hopper-to-Blackwell transition also shows how the AI chip roadmap has changed. Older GPU roadmaps could lean heavily on benchmark uplift. Modern data center chips have to answer a messier set of questions:

1. Can the platform keep latency predictable when demand surges? Average throughput is not enough. Production AI systems fail in the tail.

2. Can memory and interconnect handle larger context windows and model parallelism? Bigger models stress the entire system, not just compute units.

3. Can the software stack hide enough complexity without trapping teams in brittle abstractions? Frictionless is great until it becomes opaque.

4. Can the cluster run hot without becoming operationally ridiculous? Performance per watt is now a user experience issue for infrastructure teams.

5. Can buyers actually get capacity when they need it? A great chip that cannot be deployed on schedule is a roadmap liability.

That last point is not glamorous, but it is where real customers live. The future of Nvidia data center chips will be shaped by performance, yes, but also by supply, packaging, networking, and whether enterprises can translate capex into actual model throughput.

Blackwell’s 1-trillion-parameter support capacity is not a promise that every company should run a trillion-parameter model. Most should not. The better reading is that Nvidia is designing for the outer edge of model scale while pulling the rest of the market along behind it. Frontier labs push the ceiling. Enterprise buyers inherit the tooling.

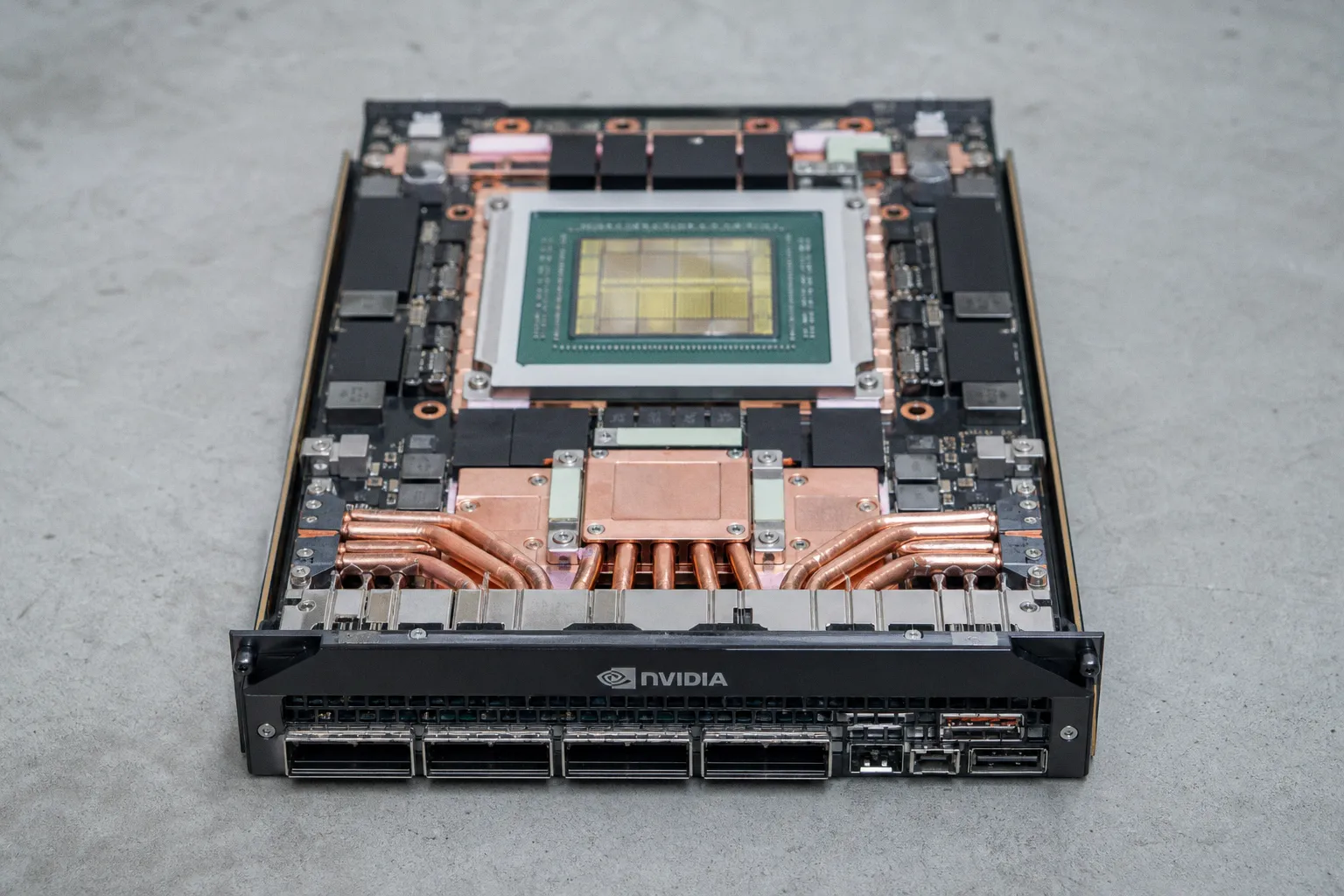

The hidden product: networking, memory, and the cluster

The chip is the easiest thing to talk about because it has a name. H100. B200. GB200. Nice, compact, searchable. But the actual data center product is the cluster.

This is where Nvidia’s 2020 acquisition of Mellanox looks less like a supporting move and more like a core chapter. High-performance AI workloads are not polite single-GPU tasks. They spray data across accelerators. They punish weak interconnects. They turn networking into a model performance issue.

NVLink is part of that story. Nvidia cites 900 GB/s bidirectional bandwidth for NVLink, and that number matters because distributed AI is full of communication overhead. If GPUs spend too much time waiting on each other, expensive silicon becomes expensive furniture.

From a developer’s chair, cluster quality shows up in strange ways. The same model can feel crisp in one environment and oddly sticky in another. Training can scale neatly to a point, then flatten. Inference can look strong under a demo load and wobble when real users arrive. The hallucination rate may get blamed on the model, but the product experience often degrades first through latency, timeouts, retrieval failures, or overloaded serving paths.

This is why Nvidia’s move from GPU vendor to infrastructure company feels inevitable in hindsight. Once AI workloads required thousands of accelerators working together, the value moved into the seams: interconnect, scheduling, libraries, drivers, system design, and observability. The seams are where latency hides.

The same pattern appears outside AI in other infrastructure markets. Capital flows toward the layer that reduces operational drag. In finance, for example, the recent funding around DeFi lending infrastructure reflects a similar appetite for rails rather than just front-end applications. Different market, same instinct: investors and users reward the systems that make the next layer easier to build.

For Nvidia, the “rails” are increasingly physical. GPU boards. Switches. Interconnects. Rack-scale systems. Software. Cooling assumptions baked into platform design. The product is no longer something a developer installs. It is something a data center absorbs.

The AI chip race is becoming a data center design race, and that is a very different sport.

That is also why simple comparisons between individual accelerators can mislead. AMD’s MI300 series, Google’s TPUs, and AWS Trainium and Inferentia are real alternatives in specific contexts. Nvidia does not have a total monopoly on AI hardware. But the question buyers ask is rarely “which chip has the best isolated metric?” It is “which platform gets my workload into production with the least friction and the most predictable scaling?”

That question favors ecosystems.

Cooling is now part of the roadmap

The more dense the rack, the less romantic the hardware story becomes. At a certain point, the limiting factor is not whether a chip can compute. It is whether the facility can feed it power and remove heat fast enough.

Modern AI data centers using high-end Nvidia hardware increasingly rely on liquid cooling, especially for dense systems such as GB200 NVL72-class racks. That does not mean every AI data center has abandoned air cooling. Many lower-density environments still use it. But the direction is clear: high-density AI infrastructure is forcing cooling into the foreground.

This changes the buyer experience. In the old server world, a company could think in relatively modular terms: buy hardware, rack it, cable it, cool it within known facility constraints. With current AI clusters, the rack is no longer an afterthought. It is a thermal and electrical commitment.

The practical questions get blunt:

- Can the facility support the power density? Not in a slide deck. In the actual room, with the actual power distribution.

- Is liquid cooling operationally mature for the team running it? Better thermals do not help if maintenance procedures create downtime anxiety.

- Does the cluster design match the workload mix? Training, fine-tuning, batch inference, and low-latency inference stress infrastructure differently.

- Can the organization keep utilization high enough to justify the spend? Idle AI hardware is not a trophy. It is a burn rate with fans.

- Will software teams get stable access, or will the cluster become a scheduling battlefield? Internal friction can erase hardware advantage quickly.

This is where my impatience kicks in. Too much AI infrastructure marketing still talks as if the customer buys performance in a vacuum. Nobody does. They buy deployable performance. If a platform requires new cooling, new networking assumptions, new procurement timing, and new operational expertise, then the user experience starts months before the first model runs.

Blackwell makes that explicit. The platform’s ambition is not just higher compute. It is coordinated infrastructure at rack and data center scale. That is powerful. It is also heavy. The onboarding is no longer a developer downloading a toolkit. It is an enterprise negotiating with physics.

Competition is real, but Nvidia owns the default path

The competitive landscape around Nvidia AI chips is more nuanced than fan arguments allow.

AMD is pushing with the MI300 series. Google continues to use TPUs as strategic internal and cloud infrastructure. AWS has Trainium for training and Inferentia for inference, both designed to reduce dependence on third-party accelerators and tune economics for cloud customers. Custom silicon is not a side plot. It is what hyperscalers do when demand becomes large enough to justify owning more of the stack.

Still, Nvidia has the default path. That phrase matters more than “best chip,” because defaults shape behavior. Developers start where examples work. Startups rent what investors recognize. Enterprises ask vendors what has the broadest support. Cloud marketplaces surface the familiar instance types. Hiring managers search for CUDA experience. Procurement teams prefer the platform that feels least likely to strand them.

Defaults are sticky because they reduce perceived risk.

That does not make Nvidia untouchable. Pricing pressure is real. Supply constraints can push customers toward alternatives. Hyperscalers have every incentive to promote their own silicon where it fits. Some inference workloads may not need the most expensive Nvidia systems. Specialized chips can win when the workload is stable and the software path is controlled.

But displacement requires more than a faster benchmark. A serious challenger has to attack the whole experience: compiler maturity, framework integration, observability, migration tools, cloud availability, pricing transparency, and support. If any of those layers feel rough, the buyer pays in engineering time.

Here is the uncomfortable math: the most expensive hardware is not always the costliest option. A cheaper accelerator that adds weeks of integration work, higher latency variance, or lower utilization can become more expensive in production. Teams know this. That is why Nvidia’s ecosystem advantage keeps compounding.

Verdict: Nvidia’s gaming past matters, but the data center stack is the story

The journey from GeForce to Blackwell is not a clean brand pivot. It is a long conversion of GPU parallelism into AI infrastructure, one layer at a time.

CUDA made the hardware programmable. Data center GPUs made it scalable. Hopper made Nvidia the default engine of the large language model boom. Blackwell turns the argument into a full-stack data center proposition: 208 billion transistors, support for models up to 1 trillion parameters, and claimed inference gains that speak directly to the economics of serving AI products at scale.

My verdict is straightforward: Nvidia’s lead is not just silicon. It is the reduced friction around silicon. That is harder to copy than a spec sheet and more valuable than a launch slide.

The risk is that the stack becomes so large, costly, and facility-dependent that some customers actively seek narrower alternatives. Not everyone needs frontier-scale infrastructure. Not every inference workload deserves a Blackwell-class deployment. The market will segment.

But for teams building at the sharp end of AI — the ones fighting latency, scale, utilization, and model size at the same time — Nvidia remains the cleanest default. Not the cheapest. Not the only option. The cleanest path from ambition to running workload.

And in infrastructure, the cleanest path usually wins.